Middle East Instability Pushes Up Plastic Packaging Costs, Adding Pressure on Seafood Exporters

Ongoing instability in the Middle East is increasingly affecting global supply chains for crude oil, petrochemicals, and plastic resins, leading to a sharp rise in plastic packaging costs in recent months. For seafood processing and exporting businesses, this has become a significant input cost concern, particularly amid intense market competition where selling prices are difficult to adjust in line with rising production expenses.

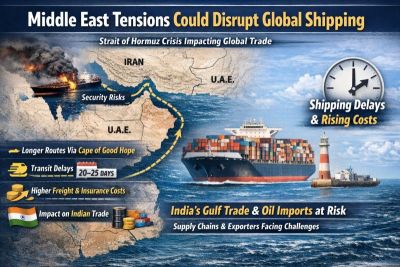

From Middle East Disruptions to Rising Plastic Resin Prices

Since the beginning of 2026, the plastic raw materials market has experienced substantial volatility due to the combined impact of oil price fluctuations, petrochemical supply risks, and disruptions in key global shipping routes. Interruptions in the flow of oil and petrochemicals through the Strait of Hormuz have tightened global chemical supplies, driving plastic and polymer prices to their highest levels in nearly four years. The Middle East accounted for over 40% of global polyethylene exports in 2025, while polyethylene (PE) and polypropylene (PP) remain key materials for the packaging industry.

In Vietnam, market observations indicate that PE prices have increased by approximately 15–30%, PP by 12–25%, and PET by 15–30% since the beginning of 2026. Vietnam’s plastics industry remains heavily dependent on imported raw materials, with imports accounting for more than 70% of supply. Plastic resin also represents a major component of production costs for plastic products. As a result, fluctuations in oil prices, resin costs, and international logistics have had a rapid impact on domestic material prices, leading to higher packaging production costs.

Domestic market observations also show that packaging-grade plastic resin prices surged significantly after the Lunar New Year. During the peak period in March and early April, prices of certain materials rose from around VND 25,000/kg to over VND 40,000/kg. Although prices have eased slightly in recent weeks, they remain substantially higher than pre-holiday levels.

Plastic Packaging: A Significant Cost Component in Seafood Processing

For seafood exports, plastic packaging is more than just a packing material. PE bags, PA/PE films, vacuum pouches, laminated films, printed packaging, carton liners, roll films, and other plastic materials are directly linked to freezing, preservation, labeling, traceability, and customer-specific delivery requirements.

According to industry feedback, packaging costs used in seafood processing have increased considerably over the past three months. Some companies reported price increases of around 25–30%, depending on suppliers, while others recorded increases ranging from 30–50%. Packaging expenses can account for approximately 3–6% of total product costs, depending on packaging specifications, with varying levels of impact across bulk frozen products, vacuum-packed items, small consumer packs, value-added products, and retail-ready goods.

The impact is particularly evident in value-added seafood products. Retail-packed, vacuum-sealed, and supermarket products typically require multiple layers of packaging, customized printing, labeling, and specifications tailored to individual customers. In contrast, bulk-packed products may reduce packaging usage, although such formats are not always suitable for consumer demand in importing markets.

Companies also face limited flexibility in stockpiling packaging materials. Seafood packaging is usually customized according to customer requirements, destination markets, and product specifications, making it difficult for exporters to purchase and store large volumes in advance.

Moreover, changing packaging specifications is not a simple solution. Customers generally prefer packaging formats that are already familiar to their markets. While larger packaging formats may help reduce material costs, they can negatively affect product presentation, retail value, and consumer convenience.

Double Pressure on Export Competitiveness

Rising packaging costs come at a time when seafood exporters are already facing multiple challenges, including raw material price fluctuations, logistics costs, stricter quality control requirements, traceability standards, sustainability demands, and aggressive price competition in export markets.

Packaging costs are especially difficult to reduce because export packaging must comply with food safety regulations, durability requirements for frozen conditions, product preservation standards, labeling obligations, and importer-specific demands.

These pressures are compounded by disruptions in global shipping. Industry reports indicate that major shipping lines have warned of rising operational costs and capacity pressure due to cargo rerouting amid risks in the Gulf region and maritime bottlenecks. Some shipping routes through the Strait of Hormuz have reportedly been temporarily suspended, while war-risk surcharges have been applied to cargo moving to and from the Middle East.

The rise in plastic packaging costs is increasingly being viewed as a significant input cost risk for the seafood industry in the second half of 2026. This is no longer only an issue for the plastics industry but has spread to packaging-intensive sectors, particularly frozen food and seafood exports.

As input costs continue to rise, exporters may benefit from stronger support measures, including improved early warning systems, easier access to imported production materials, and further reductions in logistics costs, specialized inspections, and unnecessary compliance burdens.

In an increasingly competitive export environment, controlling and reducing input cost pressures will not only help seafood companies maintain orders but also strengthen the long-term competitiveness of Vietnamese seafood in global markets.